New research by the Regional Intelligence Hub looks at the factors driving productivity differences between GCR and the West of England (WoE). The key findings are summarised in this briefing note.

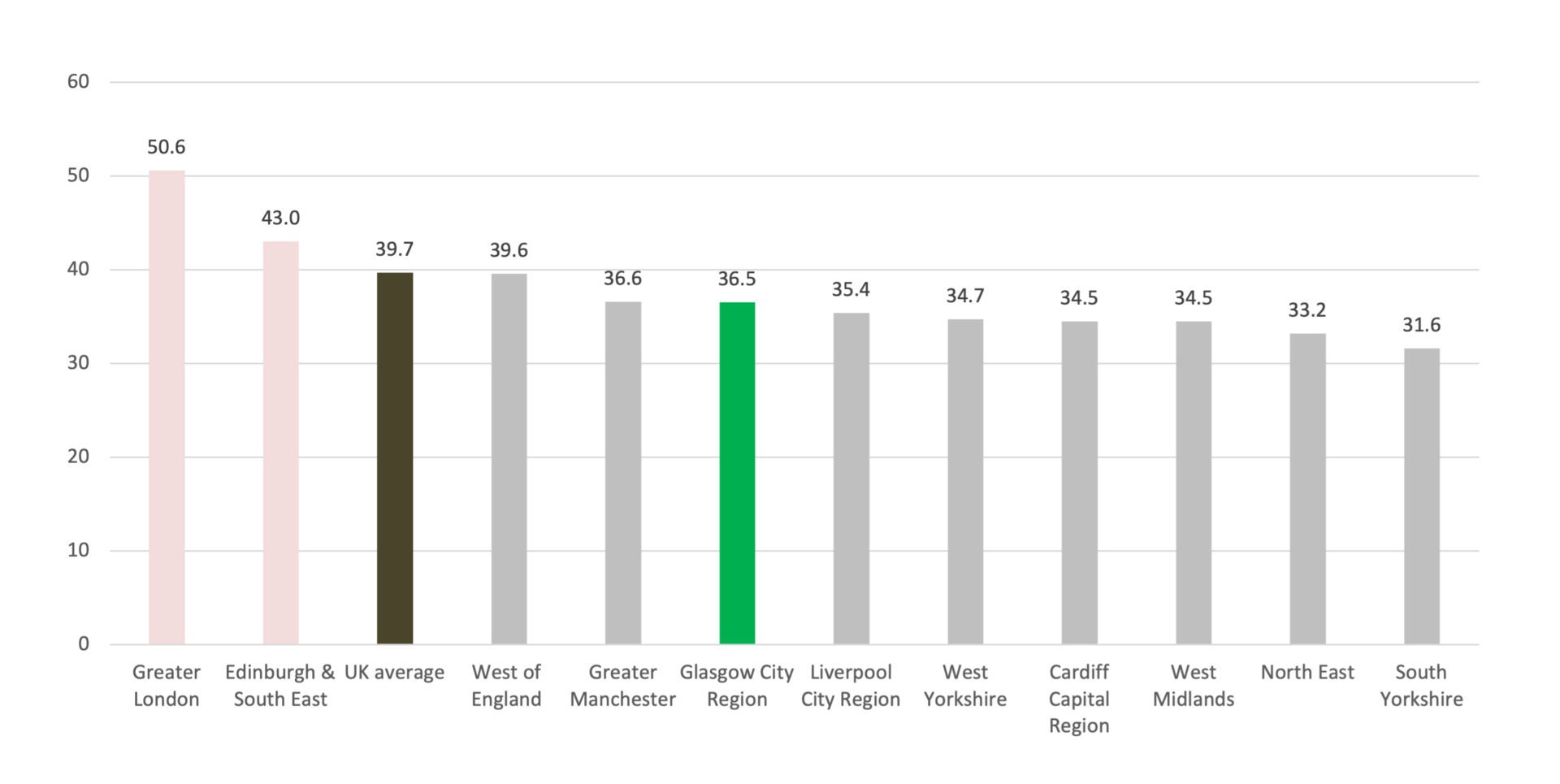

Chart 1: Gross Value Added Per Hour Worked (£), 2022

Source: ONS, Subregional Productivity statistics and BRES

*Note: Original chart has been edited to add Greater London, Edinburgh and UK average here for context

The report considers the five key drivers of productivity. The analysis concludes that productivity differences are mainly due to differences in economic structure.

The paper explores various factors as potential drivers of productivity differences. It concludes that differences are mainly attributed to:

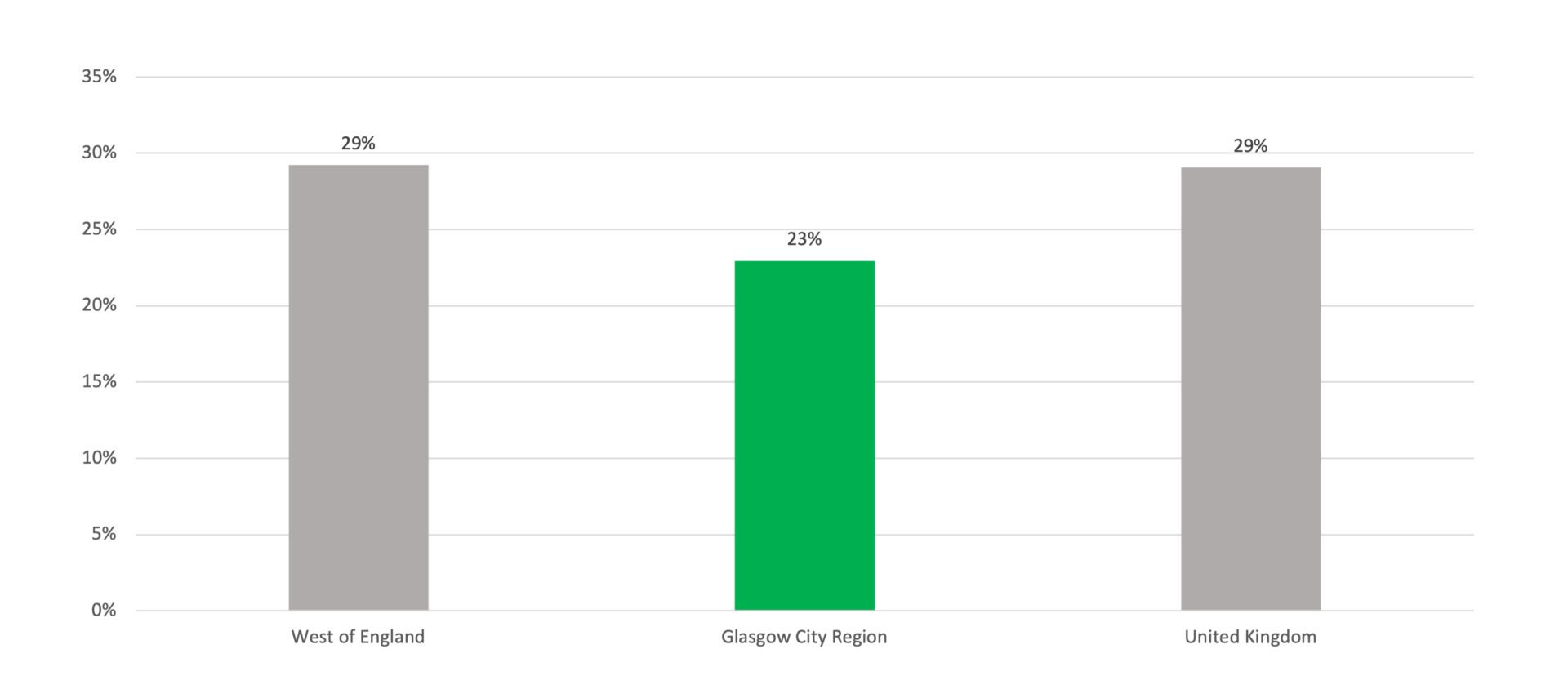

The disparity in the economic structure between the two city regions may explain some variation in labour productivity. WoE places greater emphasis on high-tech and knowledge-intensive tradeable sectors, while GCR has a stronger focus on the Foundational Economy, such as hospitality and retail.

Chart 2: Tradeable Businesses as % of Total Business Base, 2023

Source: UK Business Count, 2023

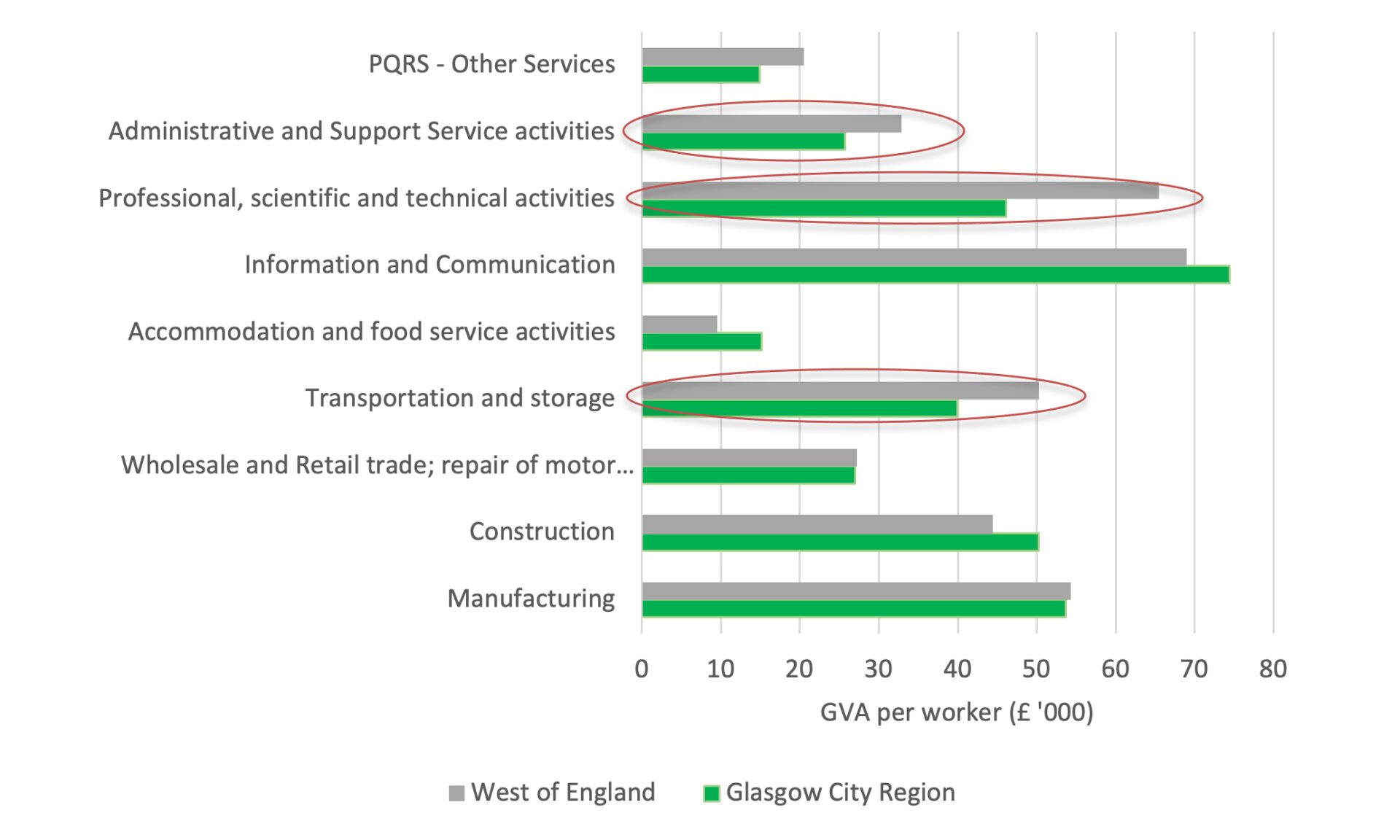

Productivity differences are driven by poor performance of some service-related sectors. The most stark difference is in Professional, Scientific and Technical Activities.

Chart 3: Average Labour Productivity by Sector, 2021 (excl. Primary Industries, Financial Services and Real Estate)

Source: Firm-level productivity distributions for Selected City Regions from the Annual Business Survey, ONS

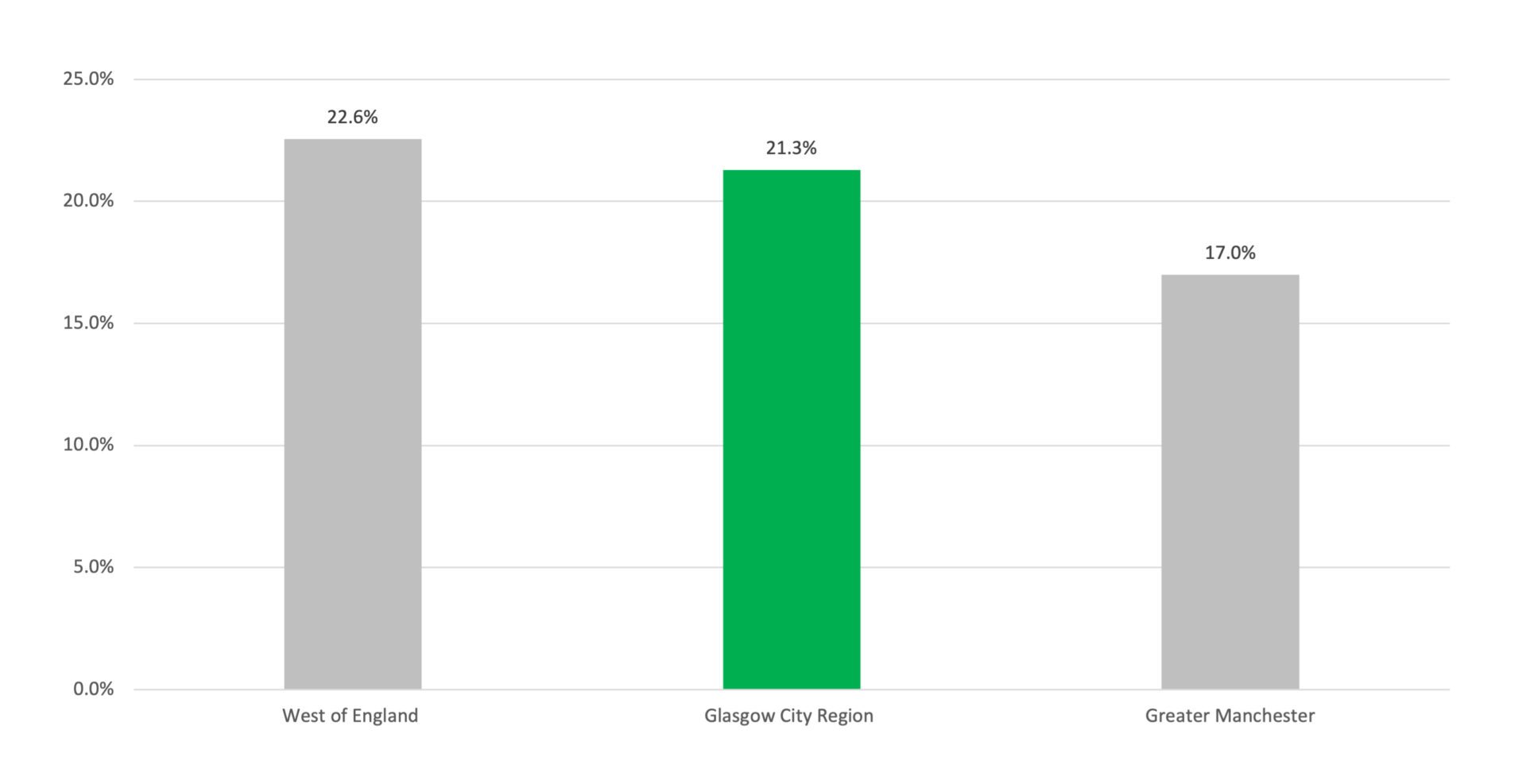

The paper looks at some key factors that are driving these productivity differences between sectors such as innovation, investment, skills and health.

Chart 4: Average Gross Investment Rate (2010-2020)

Source: Intelligence Hub analysis of ONS experimental gross fixed capital formation (GFCF) estimates by asset type, all industries.

The paper suggests that GCR shouldn’t try to replicate WoE’s economy but instead draw lessons to address weaknesses that make GCR less attractive to investors. Skills development and infrastructure should be at the core of this policy.