The latest macroeconomic data continues to show a mixed picture.

GDP

- The UK’s GDP grew by 0.2% in the three months to July 2025, a decrease from the 0.6% and 0.3% growth figures from the two previous three-on-three-month periods.

- For the first half of the year the UK was the fastest growing economy in the G7, however these periods of growth are anticipated to slow in the second half of the year and this is reflected through low business confidence. The Institute of Directors latest Economic Confidence Index fell to its lowest rating in Sep 25 since the Index began in 2016.

Labour Market

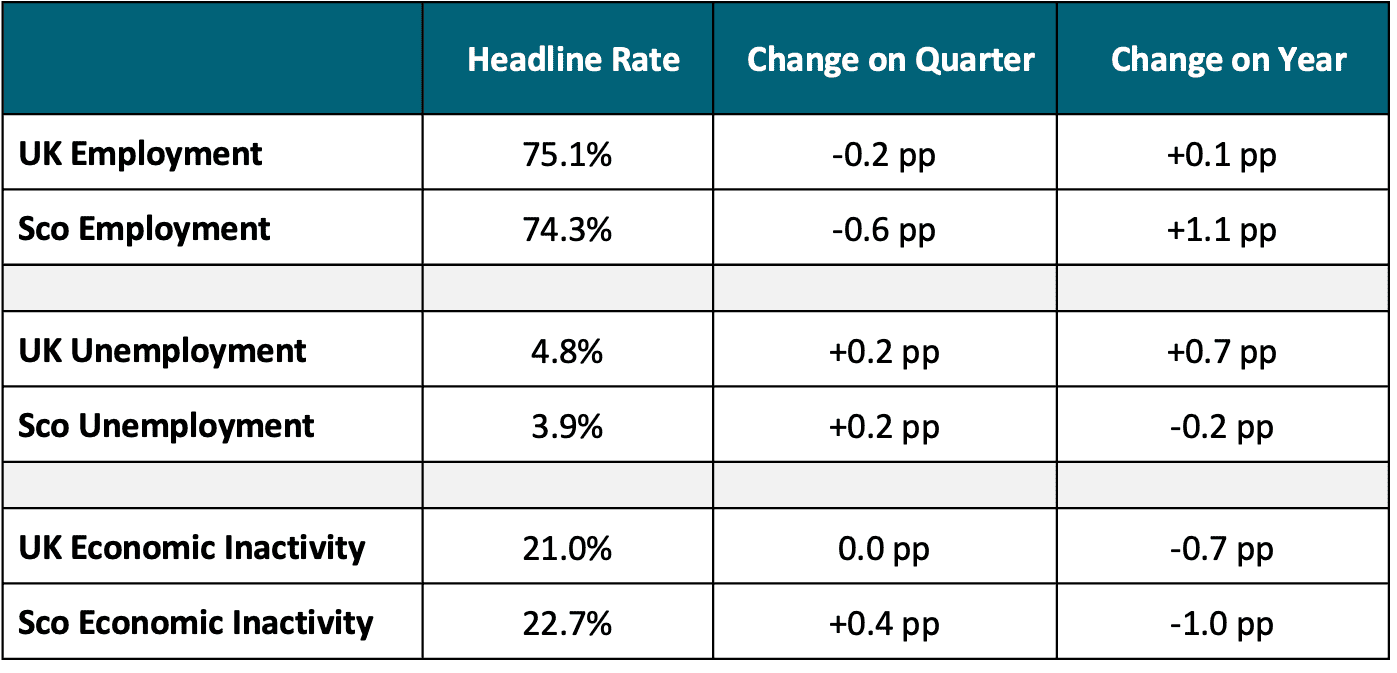

- The pessimism shown in the Economic Confidence Index aligns with a recent contraction of the UK and Scotland’s labour markets. Depending on how the Chancellor decides to meet her fiscal challenges, this may be exacerbated further after the Autumn Budget.

- Over the last quarter the employment rate decreased in both geographies, whilst unemployment and economy inactivity increased or remained the same. The latest quarter’s contraction has dampened but not fully diminished the labour market progress (UK and Scotland) since this time last year.

Chart 1: Labour market rates, Scotland and UK, June to August 2025

According to the IMF, the UK faces the worst G7 Inflation driven by profiteering.

- UK inflation has stayed at 3.8% in September.

- However, in its World Economic Outlook, the IMF predicted UK consumer prices would rise an annual 3.4 per cent this year and 2.5 per cent next, faster than other G7 countries.

- The root cause of ongoing inflationary pressure is still a contested topic amongst economists. According to the Guardian and other economic commentators, what the UK faces is profit inflation (Source: The Guardian). The Treasury takes the opposite view as it sees inflation as a result of rising import costs and wage pressures.

- The sharp rises of food prices are particularly concerning , as it disproportionately affects the poorest families. According to the industry, costs are increasing due to supply-side pressures such as regulations and the rise in the national living wage (source: FT).

Chart 2: CPI annual inflation rate, UK

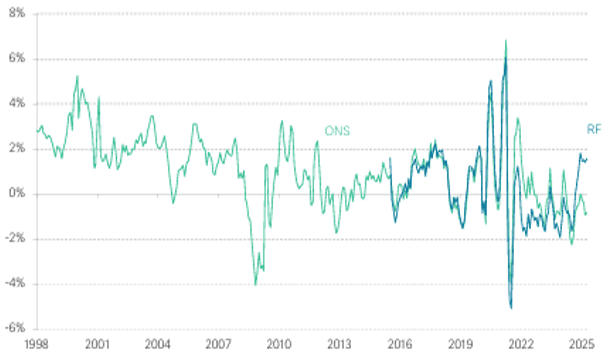

The UK has recorded a rare increase in productivity growth, according to the Resolution Foundation.

- The Resolution Foundation (RF) estimates output per hour worked rose 1.6% over past year. This is in contrast to the official estimate of 0.5%.

- The estimates are based on recently revised official estimates of GDP and figures for payroll employment drawn from tax records, rather than the official measures of hours worked drawn from the ONS’s labour force survey (the confidence problems of which have been discussed in previous briefings).

- Some economists have argued that the spike is due to recent job cuts in hospitality and retail, which were the hardest hit by April’s tax and minimum wage changes.

- There are signs of optimism too as improvements in high-value sectors such as IT and Professional Services were also noted.

- The RF warned that the short-term pick ups are not reflective of the UK’s long-term productivity problems which need to be addressed with pro-growth policies.

Chart 3: Annual productivity growth using official and RF measures of total hours worked, UK

The UK risks further worsening of living standards

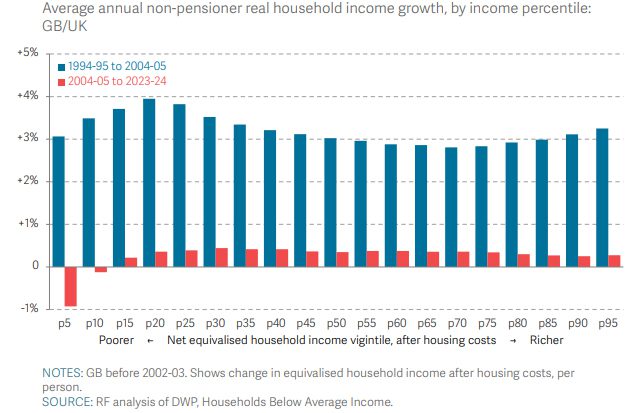

The Resolution Foundation has released a reflective report on the state of living standards in the UK over the past 20 years. It shows that income growth has stagnated to an unprecedented extent, especially in recent times.

The poorest have been disproportionately impacted

- While living standards have stagnated across all income groups, the poorest households have been hit hardest.

- Private renters have also experienced a sharp decline in living standards.

- Typical incomes have risen far more for pensioners than for working-age adults.

- The JRF projects that by 2029 average disposable incomes will be 1.3% lower than they are today – the sharpest drop in living standards since 1961.

Chart 4: Average annual non-pensioner real household income growth by earning percentile, UK

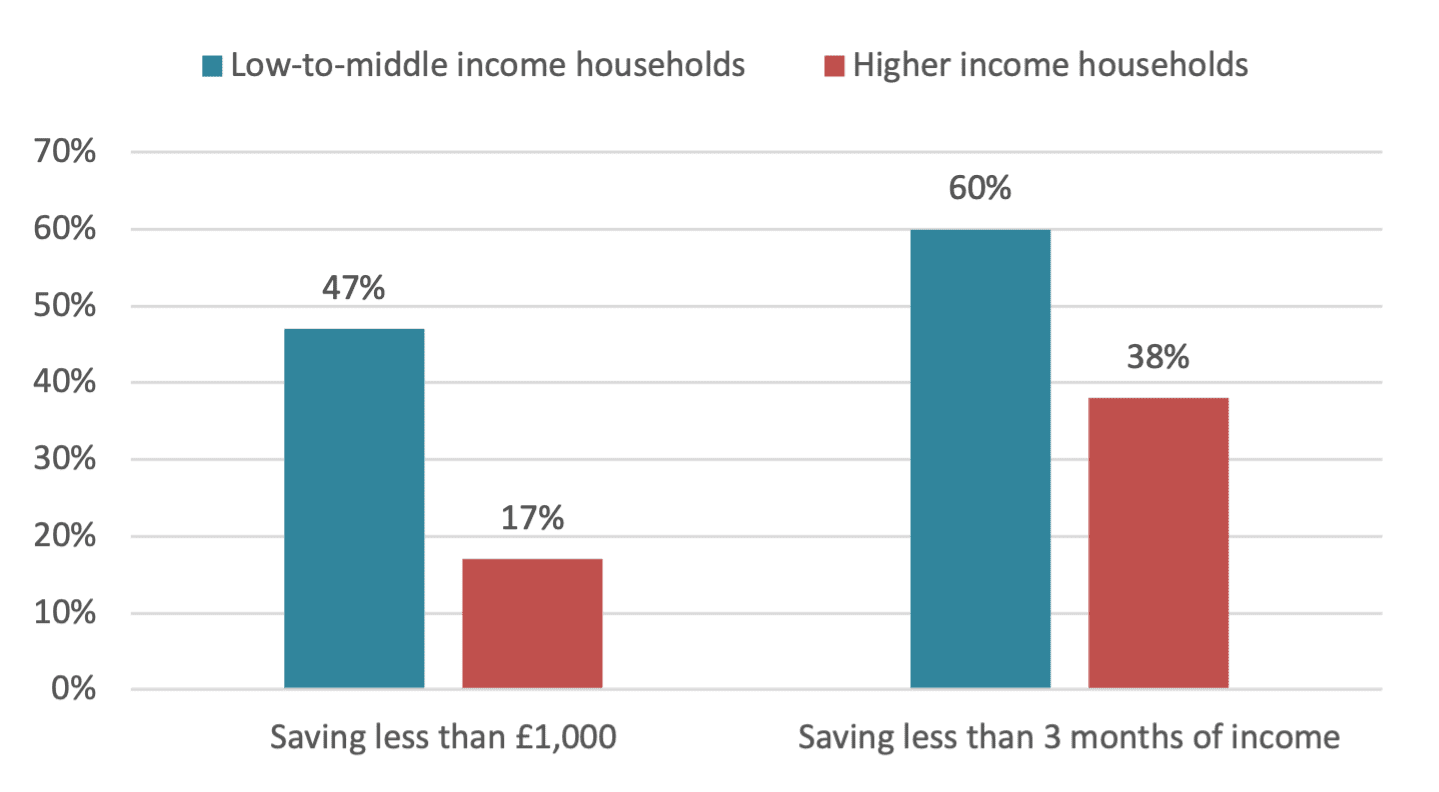

Financial Resilience of low-to-middle income households

Apart from income growth, living standards also depend on accrued debts and stocks of wealth. Savings and debt play a key role in the financial lives of low-to-middle income Britain.

- Low savings & financial vulnerability: Most working-age Britons have very limited liquid savings – two-thirds have less than three months’ income, and half of the poorest fifth have under £1,000 readily available – leaving many just a few paydays from financial trouble.

- Falling consumer debt but rising arrears: Since the financial crisis, unsecured debts have declined (especially among poorer households), but tighter credit and higher costs have led to a surge in arrears on essentials like rent, council tax, and utilities, with energy bill debts tripling since 2012.

- Policy priorities: A continued focus on living standards should be combined with targeted interventions on access to finance and support with the rising cost of essentials as well as debt-relief or advisory schemes.

Chart 5: Proportion of non-pensioner families with savings below a given threshold, by household income status: Great Britain, 2020-22

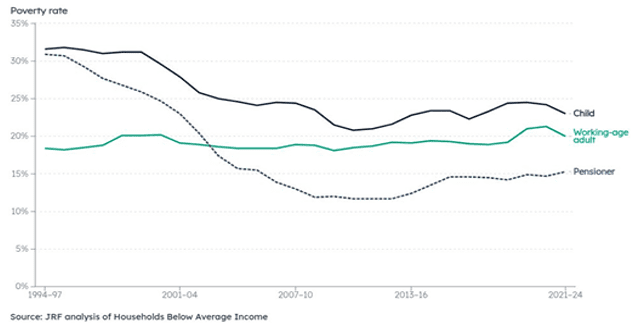

Poverty Trends

October marks Challenge Poverty Week – a time to raise awareness and call for meaningful action to end poverty.

- Poverty trends: Poverty in Scotland fell sharply from 24% in 1999–2002 to 18% in 2009–12, but has since risen to around 20% in 2021–24, though still lower than the rest of the UK due to lower housing costs and more social housing.

- Depth of poverty: The share of people in very deep poverty (below 40% of median income) increased steadily to 9% by 2019–22, representing almost half of all people in poverty, with only a brief recent decline that has not been sustained.

- Adults and pensioners: Working-age poverty increased from 18% in 1994–97 to 20% in 2021–24, peaking during the pandemic. Pensioner poverty dropped sharply from 31% to 12% (1994–97 to 2008–11) but has since risen to 15%.

- Children: Child poverty in Scotland fell until 2010–13, then rose from around 20% to 24% by 2018–21, remaining stable since. Scotland’s rate is now slightly lower than the UK average (30%), possibly due to the Scottish Child Payment, though its long-term impact remains to be seen.

Chart 6: Poverty rate for children, working-age adults and pensioners 1994-97 to 2021-24

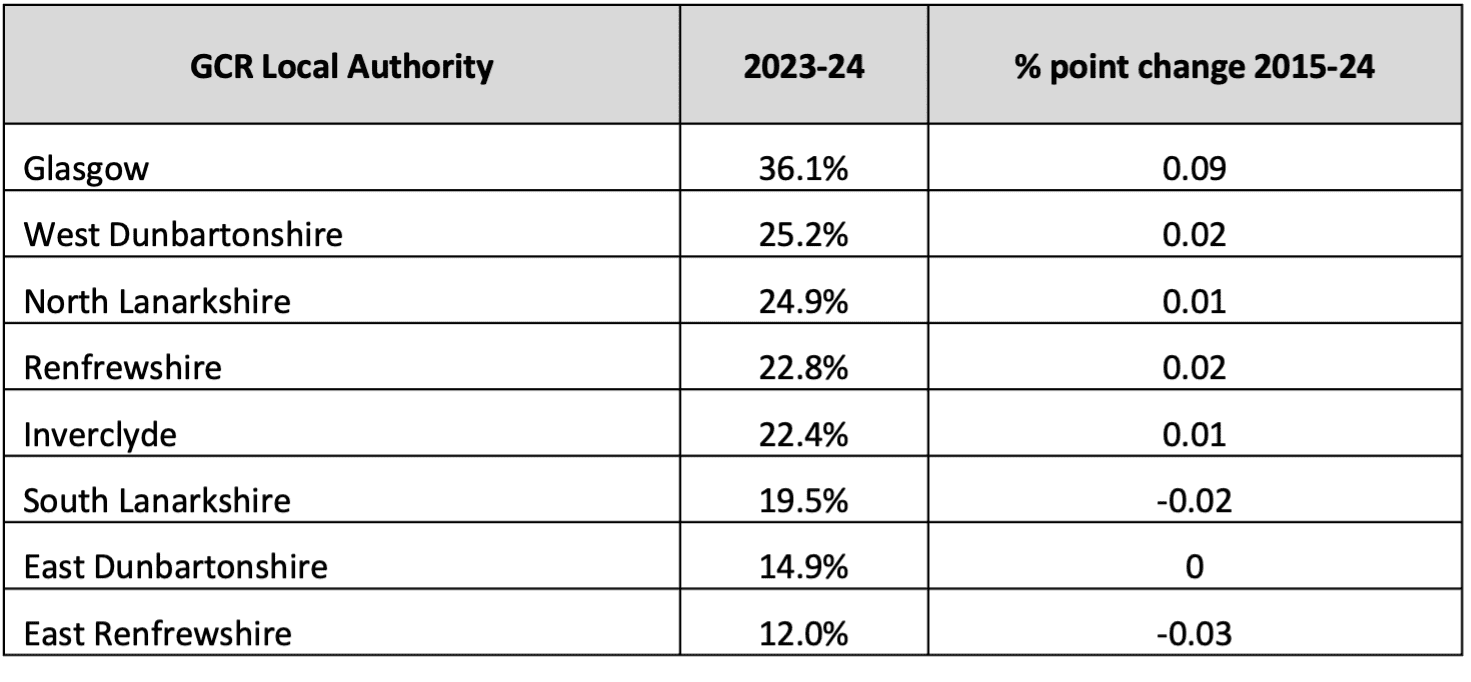

Table 1: Child poverty after housing costs, GCR local authorities 2023-24

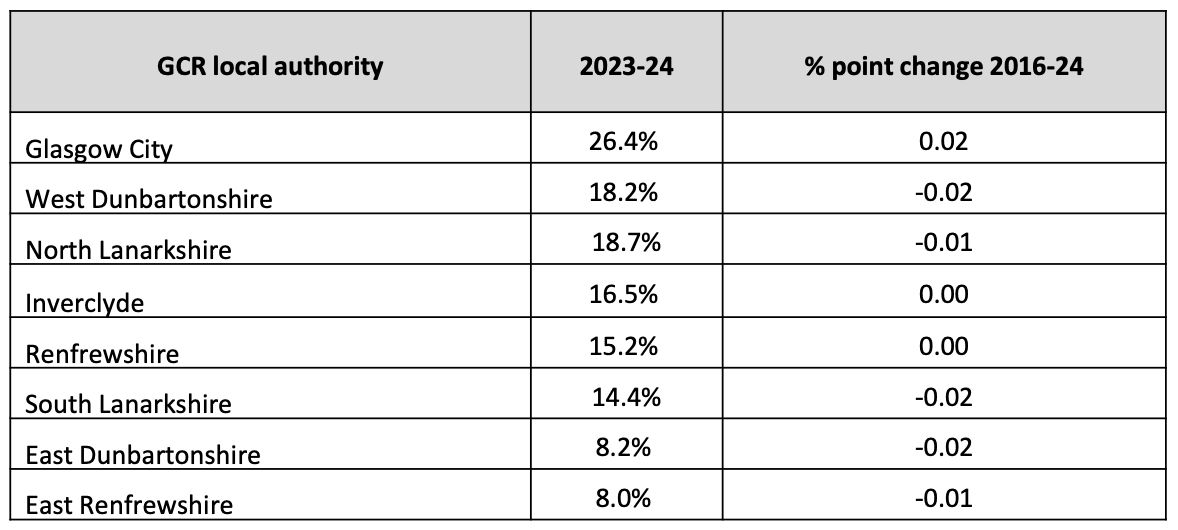

Table 2: Children in low-income families before housing costs, GCR local authorities 2023-24

Trends show the importance of policy choices

More must be done to raise incomes from work. While GCR cannot influence social security policy, we can promote fair work and support businesses that pay decent wages.

- In-work poverty: Work remains the biggest protector against poverty. However, the past decade has seen the collapse of earnings growth.

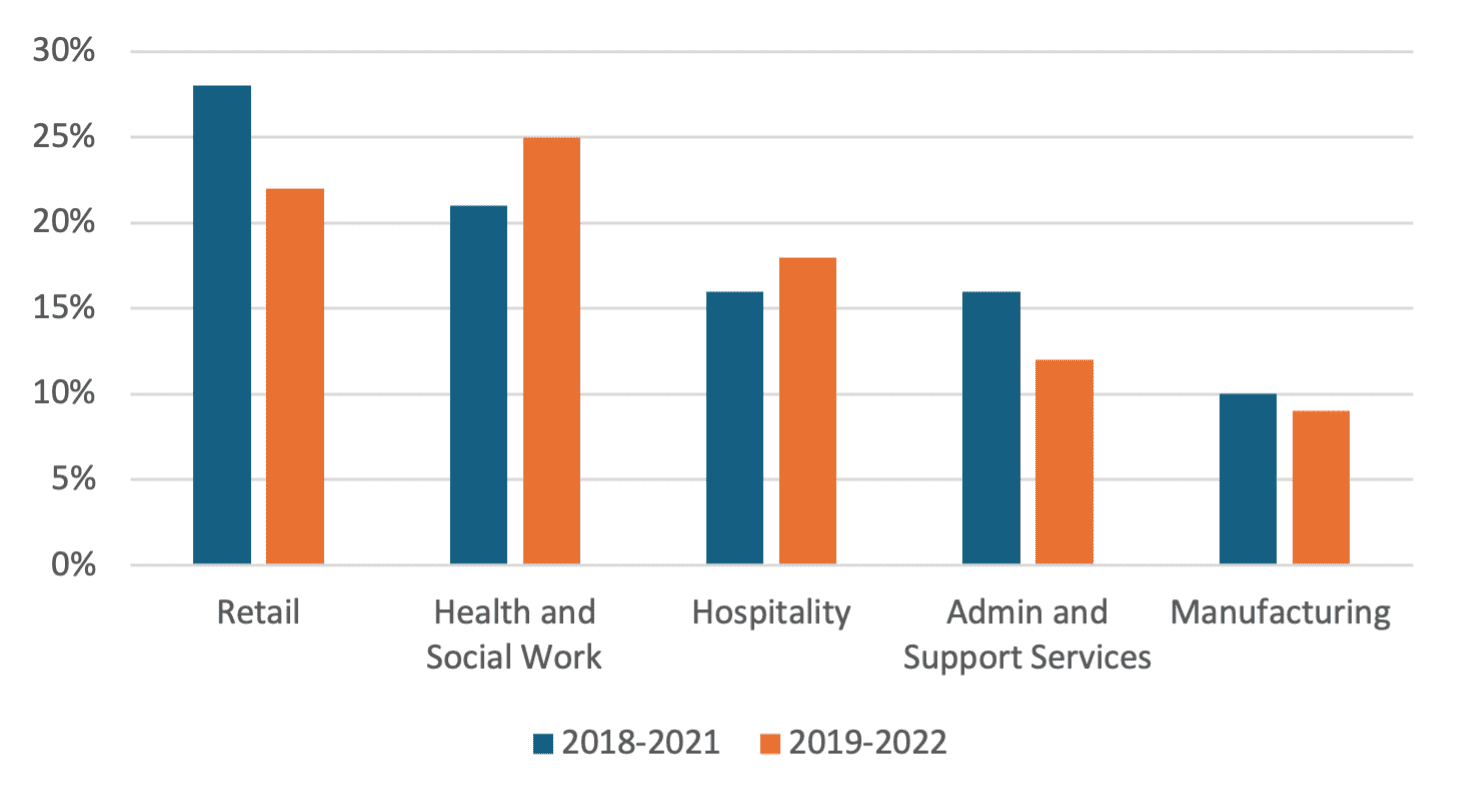

- Foundational Economy: As shown in the chart, the vast majority of people who live in poverty have someone in their family working in one of just five sectors. Although there have been improvements in some sectors, this is the part of our economy where low pay is concentrated.

- The Region has done a lot to support low-income workers through the Living Wage Campaign. More than 1,300 employers have now demonstrated commitment to the real living wage (RLW). Although this is positive, more is needed to ensure work can offer a good standard of living.

- Job Quality: The RLW alone can’t fix poor job quality, insecure hours, or instability. Policymakers must also focus on improving working conditions.

Chart 7: Proportion of people in in-work poverty where one or more people in their household work in the listed industry, 2018-21, 2019-22