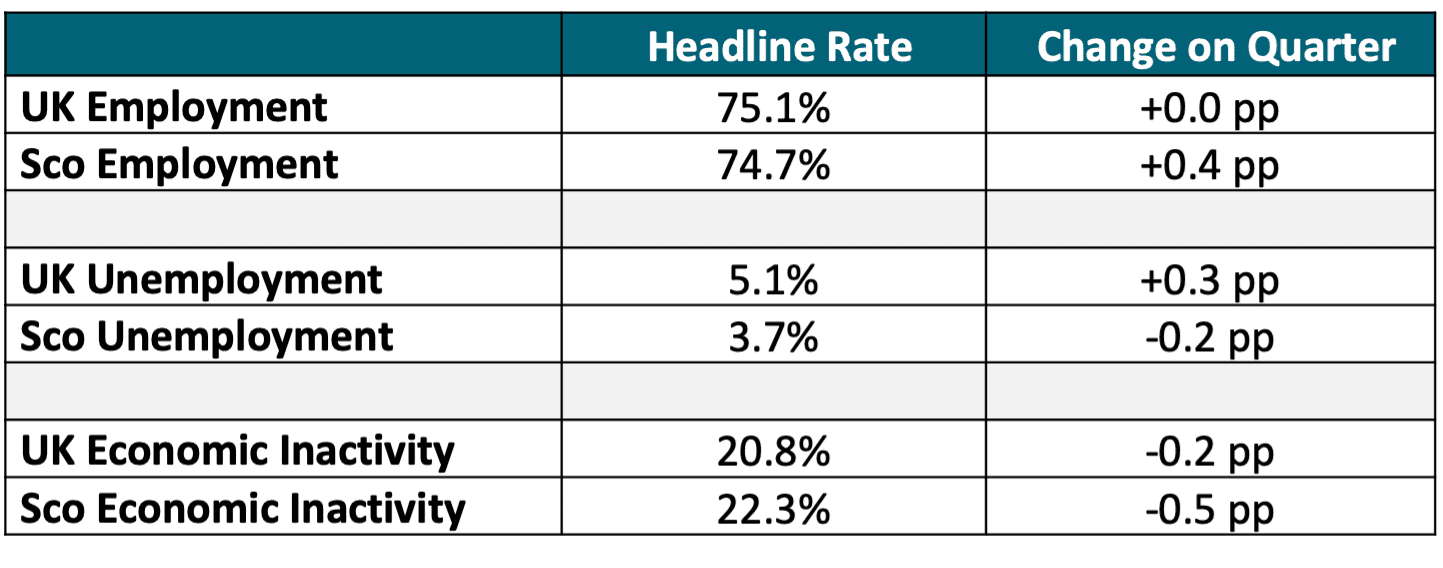

The latest economic data show relatively low levels of growth across Scotland and the UK, with Scotland’s labour market improving relative to the UK’s in Sep-Nov 2025.

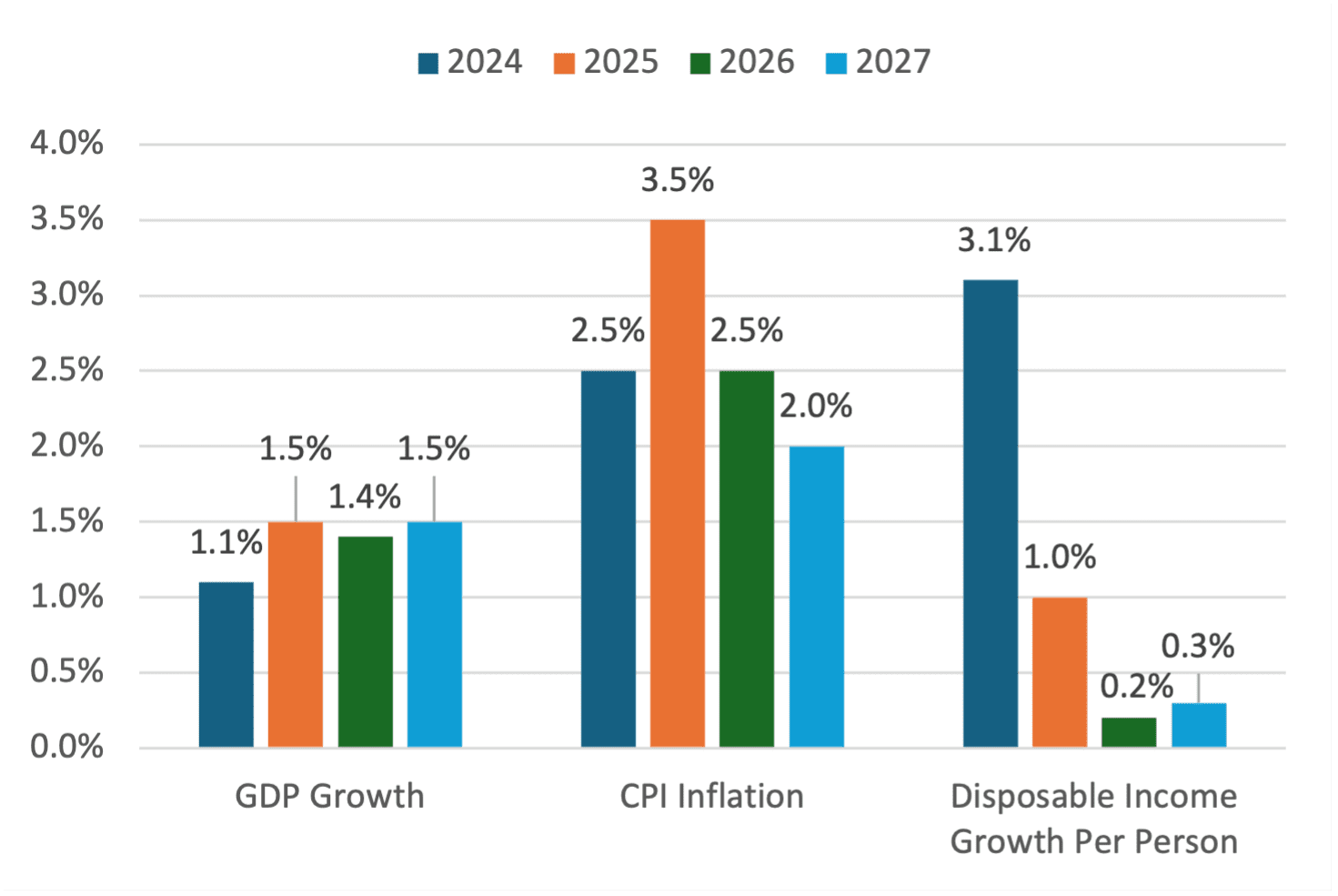

- GDP: UK GDP grew by 0.1% in Q3 (Jul-Sept) 2025. Growth was driven by services and construction (each +0.2%), while the production sector fell (-0.3%). Real GDP per head showed no growth in Q3 2025 but is up 0.9% compared with Q3 2024. Real Household Disposable Income per head fell by 0.8% in Q3 2025.

- Productivity: Labour Force Survey (LFS) estimates suggest that UK output per hour worked was 3.1% higher in Q3 2025 than pre-COVID (2019 average), with output per worker 2.1% higher across the same period.

- Inflation & Interest Rates: Consumer Price Index (CPI) inflation rose by 3.6% in the 12 months to Dec 2025, up from 3.5% in the 12 months to Nov 2025. Alcohol & tobacco and transport made the largest contributions.

- Labour Market: Labour Force Survey (LFS) estimate, as noted in chart 1, show Scotland’s labour market improving relative to the UK over the last observed quarter (Sep-Nov 2025). Increased volatility of LFS estimates mean that quarterly changes should be treated with caution.

Chart 1: Labour market rates, Scotland and UK, Sep to Nov 2025

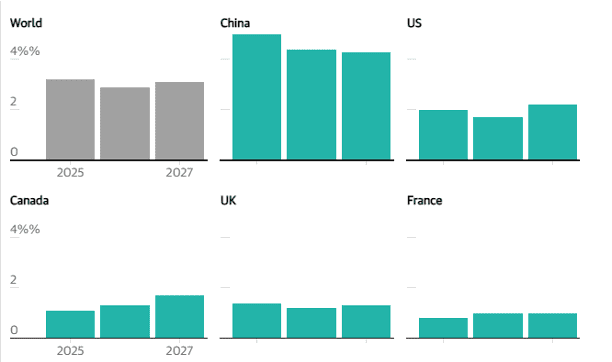

Chart 2: Real GDP Forecasts and Projections

Chart 3: Outturn and forecasts of GDP, CPI and real household disposable income per capita

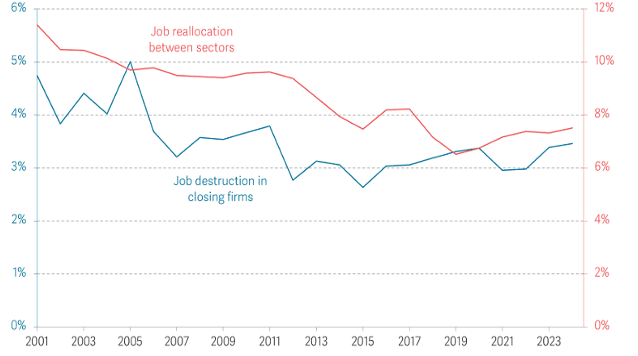

Chart 4: Job reallocation between sectors and job destruction in closing firms, UK

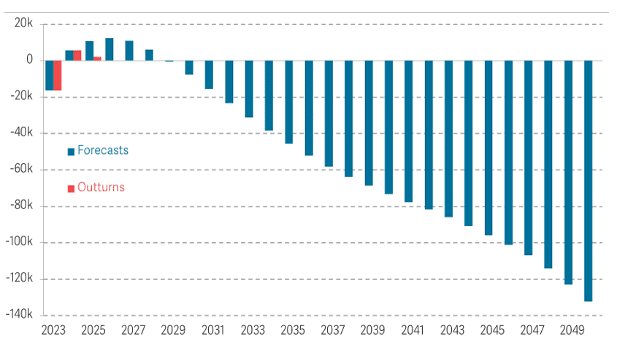

Chart 5: Outturns and forecasts of births minus deaths: UK

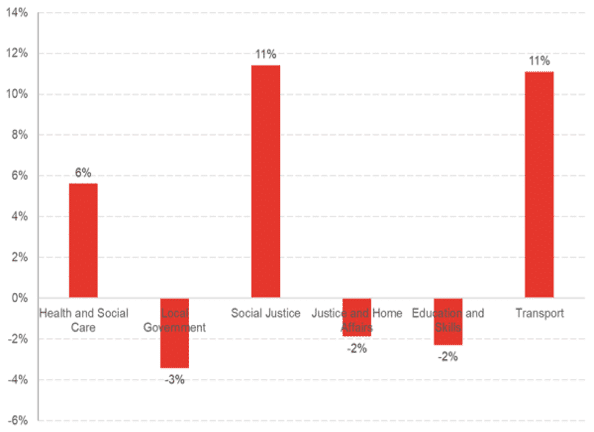

Chart 6: Spending Review- Change in Spending (Real terms) between 2025-2026 and 2028-2029

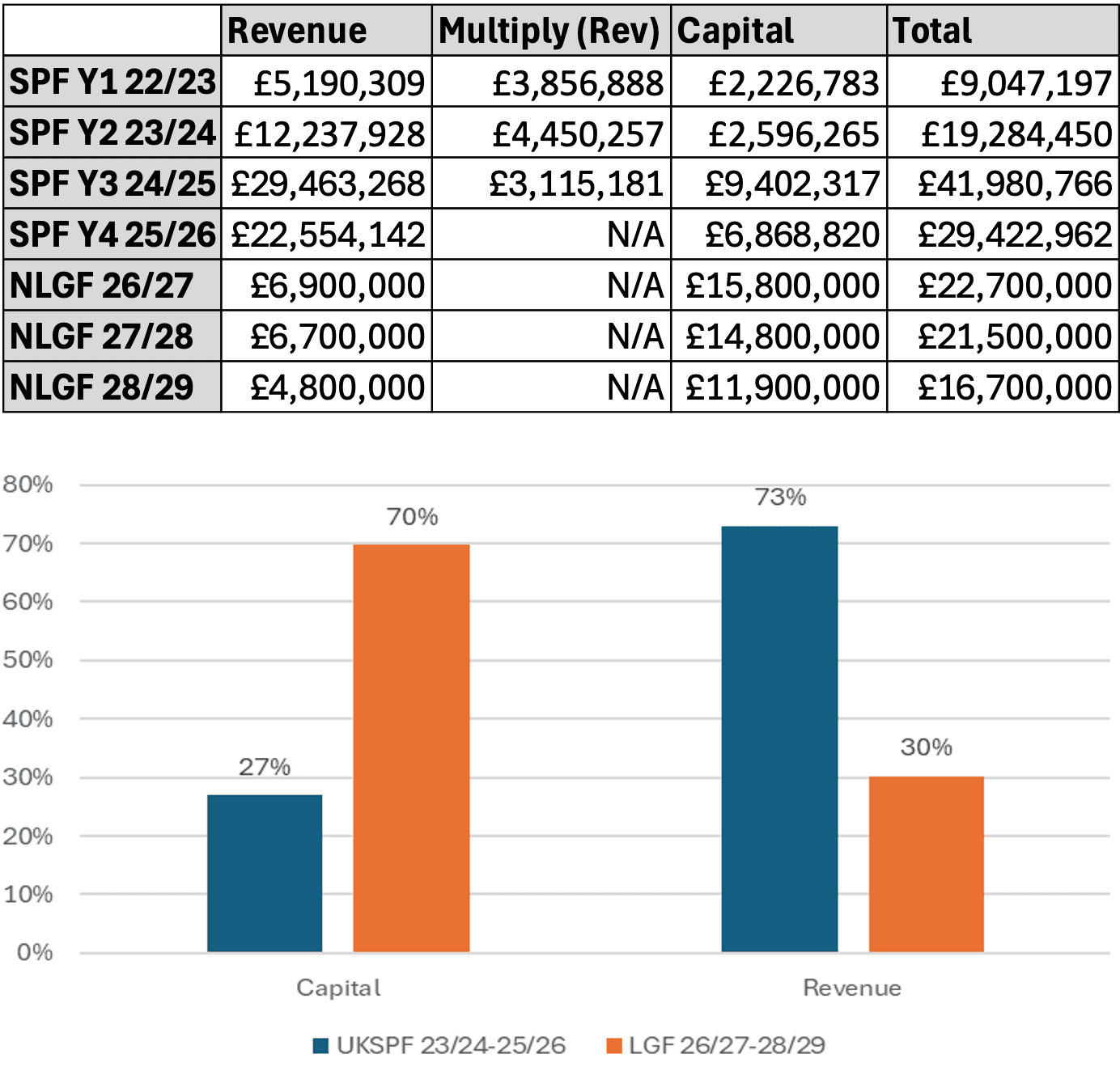

Chart 7: UKSPF and NLGF Capital and Revenue Splits