Intelligence Hub

Economic Briefing April 2026

Introduction and Key Points

This month’s briefing examines recent economic data from Scotland and the UK, alongside geopolitical challenges, and the living standards of lower-income households. It then considers how interconnected these issues are.

The latest UK and Scottish Economic Data

Economic growth remained weak at the start of 2026, with February’s modest expansion following a small upward revision to January’s previously stagnant performance. While there are some modest signs of improvement across the UK economy, conditions in the Scottish labour market are worsening. At the same time, CPI inflation has eased, although it is expected to rise again in the coming months.

Geopolitical Challenges

Rising crude oil prices could exceed the levels observed during the 2022 Russian invasion of Ukraine, with many analysts warning of a more severe economic impact if tensions in the Middle East fail to de-escalate. The IMF has also warned that the UK economy is particularly exposed to the current energy crisis, downgrading its growth forecast and predicting a rise in unemployment. At the same time, in February, Donald Trump announced a 10% tariff on all imports to the United States. These tariffs are expected to have a significant impact on trade, particularly for the Region’s manufacturing exports.

Living Standards

Rising energy and fuel costs, driven by geopolitical tensions, are likely to further strain living standards. Research by the Resolution Foundation highlights a worsening outlook for living standards among low-income groups. Glasgow City Council is looking at a Living Standards Indicator to support effective policy and decision-making. The Intelligence Hub is working with Loughborough University on this, with the view to developing it at the Regional level in the future.

Latest Scottish and UK Economic Data

The latest economic data show low levels of GDP growth for the UK, with Scotland’s labour market worsening relative to the UK.

- GDP: Monthly GDP (February 2026) grew faster than previously expected at 0.5%. This follows a revision of the January estimate to 0.1%, after earlier data suggested the economy had seen no growth in the first month of the year.

- Productivity: Labour Force Survey (LFS) estimates suggest that UK output per hour worked in Quarter 4 2025 was 0.5% lower than Quarter 4 2024, while output per worker decreased by 0.2%, compared with the same period.

- Inflation & Interest Rates: Consumer Price Index (CPI) inflation rose by 3.0% in the 12 months to Feb 2026, unchanged from the 12 months up to January 2026.

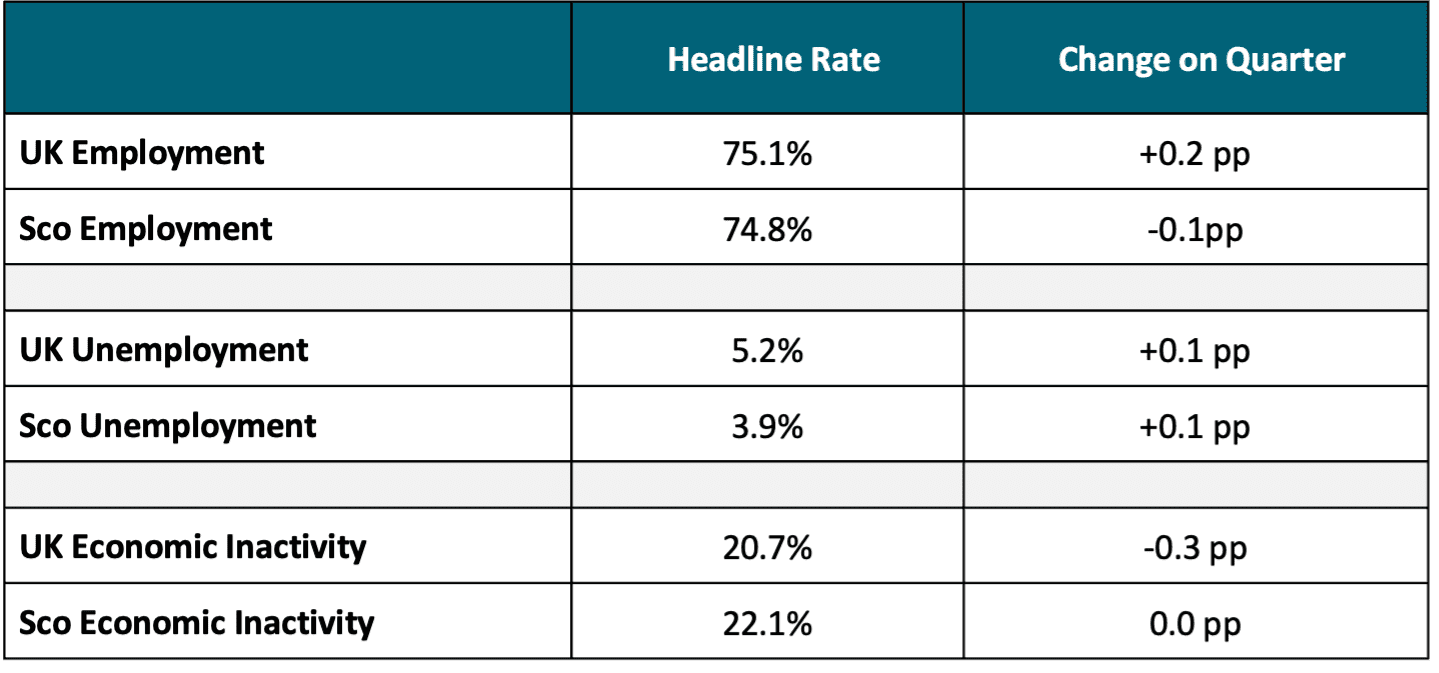

- Labour Market: Labour Force Survey (LFS), as noted in chart 1, estimates a modest worsening of Scotland’s labour market over the last quarter (November 2025 – January 2026).

Note: The increased volatility of LFS estimates mean that quarterly changes should be treated with caution.

Chart 1: Labour market rates, Scotland and UK, Nov to Jan 2026

Geopolitical Challenges

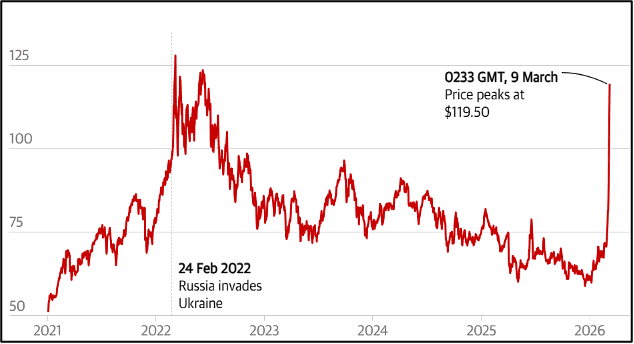

Oil Prices and UK Growth Forecast

Rising oil prices and geopolitical tensions are expected to weaken the UK’s economic outlook, with slower growth and higher unemployment forecast.

There has been a significant increase in oil prices since the outbreak of the US-Israeli–Iran conflict. Prices surged above $119 per barrel in March, the highest level since the start of the Russia–Ukraine war.

Prices have fallen since, but economists warn that a US military blockade of the Strait of Hormuz could push prices even higher, although the scale of the impact will depend on how widely the blockade is enforced and how long it lasts.

UK Growth Outlook and Unemployment

The IMF has identified the UK as one of the economies most exposed to the energy crisis linked to the conflict. It now forecasts UK GDP growth of 0.8%, a 0.5 percentage point downgrade from its January forecast of 1.3%.

This pessimistic outlook is echoed by the OECD, which has reduced its growth forecast for the UK by more than for any other G20 economy. The IMF has also raised its unemployment forecast, predicting the UK unemployment rate could rise to 5.6%, the highest level since 2015.

Chart 2: Crude Oil Prices 2021-2026

Sources: The Guardian , Financial Times

Scottish Government Report on Impact of US Tariffs on Businesses and Goods Exporters

While many businesses report little immediate impact from US tariffs, trade-intensive sectors, such as manufacturing, appear significantly more vulnerable.

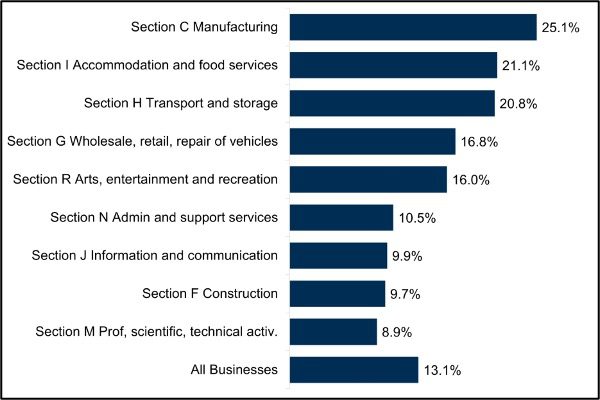

Key findings from the most recent Scottish Government Business Conditions and Insights Survey Report, a voluntary survey capturing the impact of current economic conditions on Scottish businesses, outline the impact of US tariffs on Scottish businesses:

1) Many firms unaffected or uncertain: 49.2% of exporters reported no impact and 18.8% were unsure, indicating the overall economic effect may still be limited or emerging.

2) Goods exporters are particularly affected: an estimated 32.0% of goods exporters reported impacts, compared to 13.1% of all businesses. For goods exporters, the most reported impact was additional costs at 21.1%.

3) There is an uneven vulnerability to US tariffs between sectors. Trade-intensive sectors are more heavily affected by the tariffs, with 25.1% of manufacturing firms reporting impacts.

There will likely be pressures for export-oriented manufacturing businesses in the wider GCR economy.

Chart 3: Breakdown of sectors reporting being affected by the US Tariffs in Scotland March 2026

Imports and Exports in Glasgow City Region

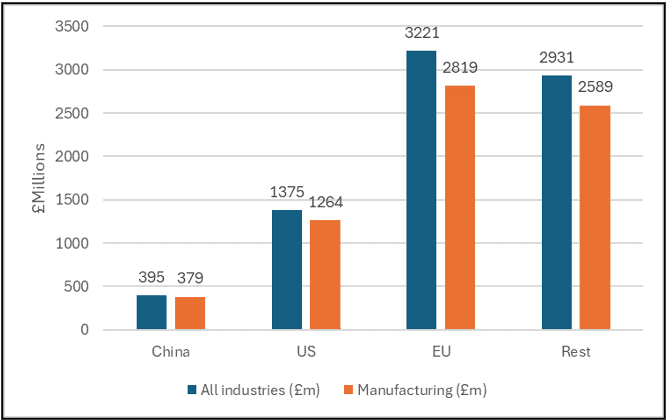

Glasgow City Region’s trade surplus in Goods and Services is a strength, but it leaves the Region vulnerable to the impacts of US Tariffs.

- Glasgow City Region is competitive globally and has a trade surplus in goods and services, meaning it sells more to other countries than it buys. This brings money into the Region and supports jobs and economic growth.

- However, this also makes the Region vulnerable to US tariffs on goods. If tariffs make exports more expensive, demand could fall, slowing down economic activity.

- Goods exports are hit harder than services because tariffs apply directly to physical products. Services aren’t directly taxed, but they are still affected indirectly, as higher costs and lower business confidence reduce investment and demand for services.

- Almost 92% of Goods exports to the US from GCR are in the Manufacturing sector, and therefore, particularly vulnerable to the impact of tariffs.

Chart 4: Glasgow City Region Goods Exports by Area 2023

Glasgow City Region’s Position to Benefit from Increased Defence Spend

Defence is a high-growth priority sector for the UK (IS-8). And in March 2026, the UK Government unveiled plans for increased defence spending in Scotland which includes a £50m UK defence growth deal announced to strengthen Scotland’s defence industry.

Glasgow City Region Context and Benefits

- The UK Government has committed to spending 2.5% of GDP on Defence. Defence is listed as one of the Government’s IS-8 sectors, representing eight sectors with the highest growth potential.

- The Government has cited long-term underinvestment in defence, the war in Ukraine, conflict in the Middle East, and the opportunity to stimulate investment through business partnerships as key drivers of this strategic shift.

- The new UK Defence Growth Deal and GCR: Funding aims to support advanced engineering, shipbuilding, and defence technology. Although some details do not appear to be finalised, it was announced that the Clyde Engineering and Innovation Centre near HMNB Clyde will receive £5 million to support work in digital systems, data science and automation.

- Previous Investment: This builds on increased investment from major companies, such as BAE Systems, which is continuing to construct advanced warships for the Royal Navy at its Glasgow site following a £4.2 billion contract. The company is also investing £300 million in its Glasgow shipbuilding facilities, including a £12 million state-of-the-art training centre to support workforce development.

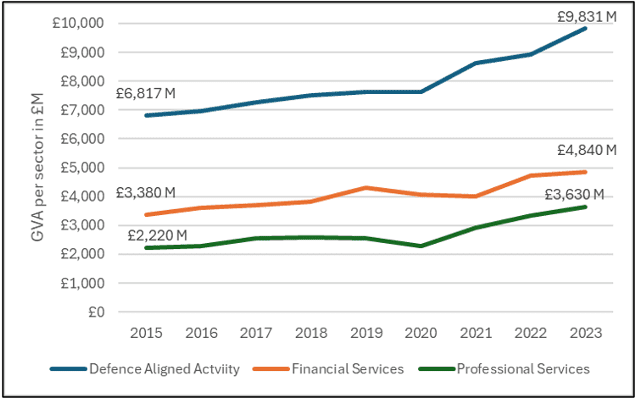

GCR’s Strength in ‘Defence Aligned Activity’

As it already makes a major contribution to the Glasgow City Region economy, it offers strong local growth potential as government spending increases.

- Economic contribution of Defence: Across Glasgow City Region economy, it is estimated that defence-related sectors support approximately 23,000 jobs across 1,725 businesses and contributes £9.83 billion to the economy.

- GCR ranks fourth among UK Core City Regions for defence exports and has the second-highest concentration of defence businesses, after the West of England.

- The contribution of Defence Aligned Activity to GVA growth is notably higher than Professional services and Financial services, both of which are also included in the IS- 8 sectors list.

- Going forward, to help support economic growth, GCR should position itself to benefit from the UK Government’s increased Defence spending such as the new UK Defence Growth Deal.

Chart 5: Glasgow City Region GVA by Sector 2015-2023 in Current Prices

Living Standards

The Impact of Geopolitical Challenges on Living Standards

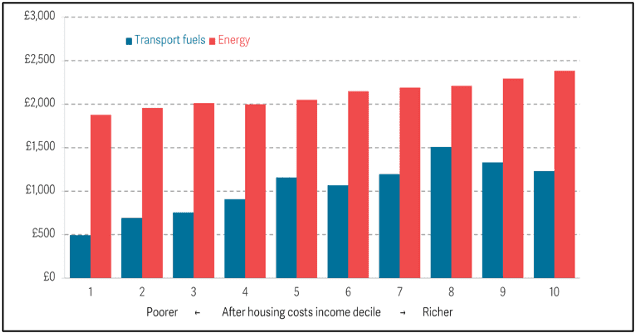

As energy and fuel prices remain volatile, policy responses to the increased cost of living should prioritise domestic energy costs over fuel duty cuts if the aim is to better support lower-income households.

The Resolution Foundation makes the case for interventions to ease the increased cost- of-living to be tailored towards domestic energy costs rather than freezing or cutting fuel duty to help the most vulnerable households.

1) Transport fuel consumption is significantly higher for higher-income households compared to lower-income households, but household energy spending is similar between the two groups.

2) Despite the rises, petrol prices are still relatively low in real terms – around the same price as pre-pandemic when adjusting for inflation.

The chancellor, Rachel Reeves, is considering measures to help households as annual energy bills are projected to approach £2,000 from July. One option is to boost the new £1 billion-a-year Crisis and Resilience Fund, run by councils in England, to provide both preventative support and crisis assistance for households.

Chart 6: Resolution Foundation’s Household spending on Transport bills and Energy bills

Downturn in Living Standards for Low Income Families

The Resolution Foundation’s new book ‘Unsung Britain’ examines how everyday families navigate income, spending, and rising living costs to shed light on their challenges.

Key Findings:

- Major slowdown in living standards growth – Incomes for the poorest half of working-age families doubled over the 40 years up to 2004–05. However, because incomes have grown much more slowly since then, it would now take more than 130 years for them to double again.

- Earnings stagnation since the mid-2000s – Most of the £7,700 increase in average household earnings for lower-income families since the 1990s occurred before 2004–05, with weak wage growth since then driving the slowdown in living standards.

- Work is no longer a guarantee of financial security – 55% of non-pensioner families in poverty now have someone in work.

Potential ways to address this downturn in living standards:

- Supply-side reforms designed to stimulate economic growth. This will enhance the returns to employment and support improvements in living standards.

- Improving pay and conditions in sectors such as social care is also proposed through ‘Fair Pay Agreements’. GCR has had recent success in encouraging employers to adopt the living wage. In its first year, the campaign exceeded expectations, securing 204 new Living Wage employers and raising pay for approximately 1,900 workers.

- Stronger enforcement of labour market rights and reforms to the benefits system. This could include linking benefits more consistently to wage growth.

Source: Resolution Foundation

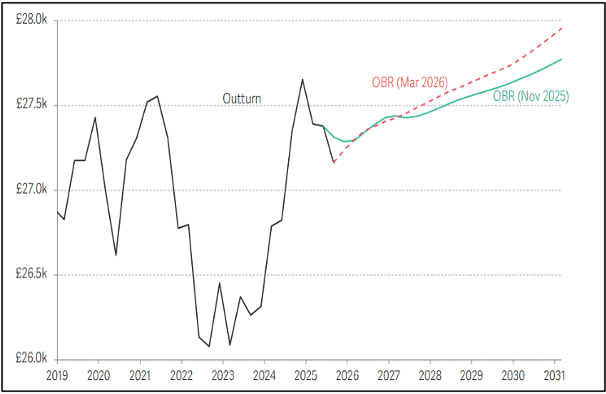

Middle East War Threatens Expected Living Standards Boost

The UK was set for a decent increase in living standards this year, and a bumper rise for lower-income families. But the new energy price shock risks ruining this good news.

Short-term improvement: Living standards in the UK were expected to rise in 2026–27, with typical working-age families gaining about 0.9% (£300) and lower-income households rising 3.9% (£800) due to benefit increases and the removal of the two-child limit.

Risks and longer-term outlook: In a separate Resolution Foundation analysis on the impact of the Middle East conflict, the energy price shock due to the war could increase inflation and add about £500 to annual energy bills, hitting poorer families hardest.

Beyond next year, living standards are expected to stagnate or fall slightly because of weak wage growth, and child poverty may rise again after an initial drop.

Possible upside: If real wages grow faster (3.5% instead of 1.4%), living standards could improve instead of falling and government borrowing could drop by up to £20 billion per year.

Chart 7 : Average real household disposable income per person (2025-26 prices): UK

Source: Resolution Foundation

A new Living Standards Indicator for GCC

Glasgow City Council has expressed an interest in developing a Minimum Income Standard (MIS). This MIS would define the level of income needed for everyone in GCC to achieve a socially acceptable standard of living. In the future, the aim is for the MIS to be replicated across Glasgow City Region.

Unlike poverty lines, which measure income deficits, MIS is a needs-based measure that shows what people require for a decent quality of life and why.

The Intelligence Hub will work with Loughborough University to develop a bespoke regional indicator. This will involve:

Adapting the national Minimum Income Standard (MIS) for GCC so it reflects local living costs and needs. This is to be trialled at the GCC level with the view to replicate for the Region.

Producing income benchmarks for different household types, including average household figures.

Using the GCC MIS as a measure of success, allowing us to track progress in living standards over time.

An MIS for GCC can provide a practical tool for policy design, monitoring, and evaluation.

Key policy implications include:

- Setting a Regional benchmark for living standards: Policymakers can use the GCC MIS to define what income is needed for a decent standard of living locally, giving a clearer benchmark than national poverty lines.

- Tracking progress and evaluating policy: The indicator can be used to monitor changes in living standards over time and assess whether policies (e.g. employment, housing) are improving residents’ ability to meet essential needs.

- Targeting support more effectively: By identifying which household types fall furthest below MIS, policymakers can better target interventions such as income support, childcare provision, or employment programmes.

- Shaping housing and cost-of-living policies: Because MIS reflects the real cost of essentials, it can highlight the impact of housing, transport, and childcare costs and support policies that reduce these pressures.

Contact

For queries, please contact: Joseph.McGlynn@glasgow.gov.uk

The Scottish Budget

The 2026-27 Scottish Budget, published on 13th Jan 2026, highlighted further fiscal challenges ahead nationally and locally; considerably greater than had been forecast in June.

Tax: The primary tax announcement was a tax-rise, with freezes to the top three income tax thresholds until April 2029 bringing more people into these bands through fiscal drag. While two new council tax bands were introduced for properties over £1m (mirroring UK Government policy), a variety of commentators have highlighted there remains no sign of a much-needed revaluation of council tax.

Spend: Despite additional borrowing and attempts to plug gaps with one-off funding pots, still having to make substantial cuts, owing to weaker underlying tax forecasts from the Scottish Fiscal Commission (with forecast Income Tax down by £274m for 2026-27 compared with 2024).

- Revenue Spending: Relative to plans laid out in June, day-to-day spending has been cut by £480m. Planned increases in day-to-day spending are very small – 0.6% over inflation in 2026-27 and 0.2% above inflation on average over the following two years. Local Government and Finance is set to see a 2.1% real terms reduction per year.

- Capital Spending: Plans for capital spending have also been curtailed by 10% (£860m) for next year relative to June’s outlined plans.

Source: IPPR Scotland, IFS, FAI

The Scottish Budget: Challenges for Local Government

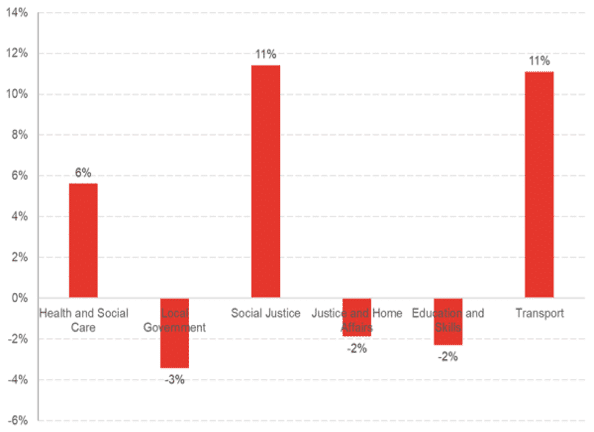

The Spending Review highlights that maintaining current service levels for local government will be very challenging.

- Health & Social Care spending is projected to grow by around 6% in real terms over three years (effectively health-only, as regular transfers to local government are excluded).This is below the Scottish Government’s May Medium-Term Financial Strategy assumption of 3.3% real-terms annual growth to meet demand.

- The local government settlement is highly constrained over the three years, particularly given rising social care demand.

- The budget assumes significant, but unspecified, efficiency savings based on local government reform, with limited detail provided on how these savings will be delivered.

Source: FAI

Chart 6: Spending Review- Change in Spending (Real terms) between 2025-2026 and 2028-2029

Source: Scottish Fiscal Commission

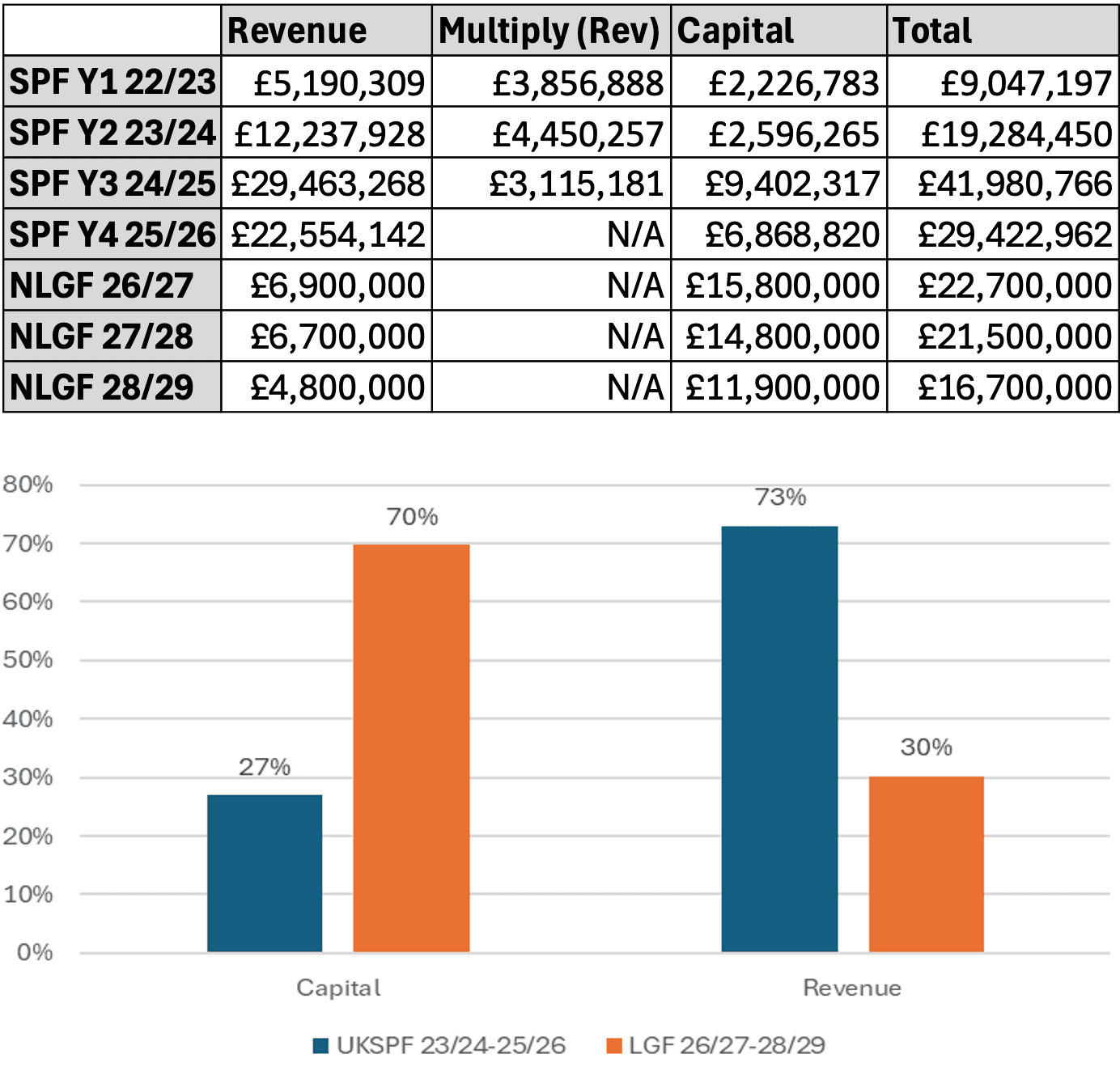

The budgetary challenges facing Local Government have also been compounded by a reduction in revenue funding as UK Government migrates from the UK Shared Prosperity Fund into the New Local Growth Fund.

- The UK Shared Prosperity Fund (SPF) was introduced by the UK Government in 2022 as a post-Brexit successor programme to EU Structural Funds, with a commitment to match the level of funding received from Europe.

- Over the last three years GCR received approx. £91m of funding from SPF. Through the UK Gov’s transition into the New Local Growth Fund (NLGF) the amount awarded to the Region decreased by 33%.

- This cut will have a significant impact on how the Region’s member authorities (MAs) deliver employability and business support services.

- The challenge for MAs is exacerbated by the proportions flipping within NLGF to be dominated by Capital spending.

Chart 7: UKSPF and NLGF Capital and Revenue Splits

Source: UK Government

The Scottish Budget: Misalignment with Goals

IPPS highlight a credibility gap caused by the poor alignment between the Budget and shared national and regional goals of reducing child poverty, improving public services, growing the economy, and addressing the climate emergency.

- Child poverty: The UK Government’s removal of the 2-child limit saved SG around £125m, but the Budget revealed little detail around whether this would be spent on child poverty reduction measures, or how much additional spending is included in measures such as the £50m Whole Family Support package or £49m boost to the Tackling Child Poverty fund.

- Addressing the Climate Emergency: Much of the £5bn identified as ‘climate positive spend’ includes items requiring investment regardless, including rail (£1bn) and affordable housing (£0.9bn). It is business-as-usual for spending on areas with negative climate impact, increasing by £110m, including extending the capacity of the A9 and A96. Clean heat spending proposals have been scaled down considerably, from a committed £1.8bn to £1.3bn over the next four years.

- Improving public services: There is consensus that it is very challenging to maintain, let alone improve, the quality of public services in light of extremely tight settlements, as outlined in the previous slide. Local government faces funding cuts of 2.1.% per annum in real-terms. This would require increases in council tax of 8% to hold budgets constant. The Christie Commission’s recommended shift towards preventative spending seems increasingly remote.

- Economic Growth: While cuts to business rates for retail, hospitality and leisure are welcome, economic growth is challenged too by announced cuts from the Scottish National Investment Bank and Scottish Enterprise.

Source: IPPR Scotland, IFS

Further Information

For queries and further information, please contact Christina Kopanou: